Customer needs are rapidly changing. To meet those needs, banks need to make customer experience the starting point for process design.

Supports leading financial institutions on strategy, sales and distribution, risk management, and operations effectiveness. Brings deep expertise in branch sales productivity, collections, and next-generation operating models for banks

Helps transform banks and non-banks across a broad range of topics to sustainably drive revenue growth and to enhance efficiency.

June 20, 2019 Today, deep within the headquarters and regional offices of banks, people do jobs that no customer ever sees but without which a bank could not function. Thousands of people handle the closing and fulfillment of loans, the processing of payments, and the resolution of customer disputes. They figure out when exceptions can be made for customer approvals and help the bank comply with money laundering rules, to name but a few.

In ten years, back-office operations will look starkly different. For starters, far fewer people will be needed. McKinsey estimates that 75 to 80 percent of transactional operations (e.g., general accounting operations, payments processing) and up to 40 percent of more strategic activities (e.g., financial controlling and reporting, financial planning and analysis, treasury) can be automated. Operations staff will have a very different set of tasks and thus will need different skills. Instead of processing transactions or compiling data, they will use technology to advise clients on the best financial options and products, do creative problem solving, and develop new products and services to enhance the customer experience. Banks, in other words, will look and feel a whole lot more like tech companies.

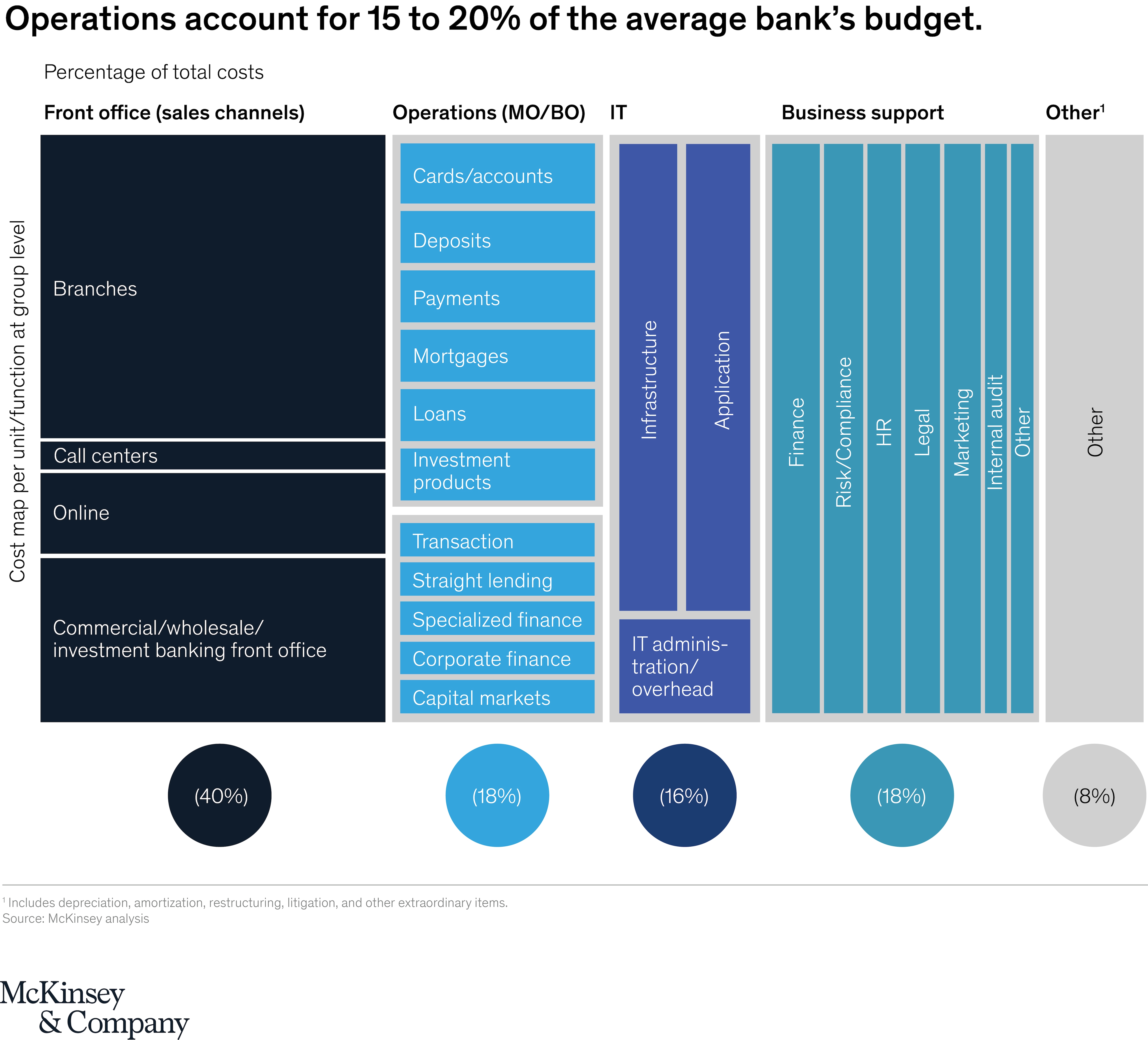

Financial institutions need to do big picture, board-level thinking about how to prepare for the revolutionary impact digital technology will have on banking operations. With operations consuming 15 to 20 percent of a bank’s annual budget (Exhibit), transforming these functions will lead to significant improvements in profitability and return more capital to shareholders. It can also boost revenues by enabling banks to provide better products and services to customers.

Today, many bank processes are anchored to how banks have always done business—and often serve the needs of the bank more than the customer. Banks need to reverse this dynamic and make customer experience the starting point for process design. To do so, they need to understand what customers want, and how and when they want it. Instead of a major cost center, operations of the future will be a driver of innovation and customer experience.

Based on our work with major financial institutions around the world and from McKinsey Global Institute research on automation and the future of work, we see six defining characteristics of future banking operations.

Today, banks offer standardized products hardcoded with specific benefits, parameters, and rules–30-year mortgages, travel rewards credit cards, savings accounts with minimum balances. A variety of operational roles are charged with supporting these products and managing the rules governing them. In future, these activities will be automated, and employee roles will shift toward product development. Instead of evaluating credit risks and deciding on mortgage approvals, operations staff will work with automated systems to enable a bank to offer its customers flexible and customized mortgages.

Imagine, for instance, a bank launching a new credit card in which the card member gets to define the rewards points they can obtain–perhaps 30 percent of rewards going to an airline, 30 percent as cash back, and 40 percent at a specific retailer. Or maybe a bank decides to offer loans that allow customers to specify their repayment plan and due dates. Today, these scenarios would be a nightmare for banks to orchestrate—each card or loan would almost require its own operations team. But soon, operations will use their knowledge of bank processes and systems to first develop customized products and then leverage technology to manage and deliver them.

Automation and artificial intelligence, already an important part of consumer banking, will penetrate operations far more deeply in the coming years, delivering benefits not only for a bank’s cost structure, but for its customers. Digitizing the loan-closing and fulfillment experience, for instance, will speed the process and give customers the flexibility and freedom to view and sign documents online or with their mobile app. Typically, US consumers have to wait at least a month to get approval for a mortgage—digitizing this process and automating approvals and processing would shrink wait time from days to minutes.

Same for call centers. Instead of waiting on hold or being pinballed between different representatives, customers could get instant, efficient automated customer service powered by advanced AI.

AI and advanced analytics could also improve dispute resolution. Customers can contact their bank any time through internet, mobile, or email channels and receive quick, real-time decisions. On the back end, systems would perform almost instant data evaluation about the dispute, surveying the customer’s history with the bank and leveraging historical dispute patterns to resolve the issue.

Today, many operations employees perform dozens or even hundreds of similar tasks every day–reviewing customer disputes on credit or debit cards, processing or approving loans, making sure payments are processed properly, and so on. It’s not surprising errors happen. At some US banks, we have seen up to five to ten percent of all debit card disputes processed with errors.

Automating these and other processes will reduce human bias in decision-making and lower errors to almost zero. This will give operations employees time to help customers with complex, large, or sensitive issues that can’t be addressed through automation. And these employees will have the decision-making authority and skills quickly resolve customer issues.

The use of predictive analytics can dramatically improve the management of operations in several ways. First, it enables operations leaders to be more precise and accurate in their predictions. Instead of using simple arithmetic based on a limited number of variables to predict demand, demand predictions for specific products and services can be made based on granular profiles of customer segments and customer behavior using dozens or hundreds of variables. Banks can build detailed profiles from a multitude of data sets–including online interactions, geographic information from cell-phone usage, and aggregated payments behavior–and then apply analytics to predict the needs and desires of their customers—down to the level of a single individual in some cases.

Comprehensive data sets will also enable managers to set more KPIs. For example, instead of tracking just average handle times and customer satisfaction at a call center, banks could drill down to see how much time millennials or residents of a particular state spend on the phone with reps. If they spend longer than average, banks can determine why and, if needed, change how they communicate with these customers or adjust products or services to better serve them.

Finally, applying analytics to large amounts of customer data can transform issue resolution, bringing it to a deeply granular level and making it proactive not reactive. Instead of a bank addressing an error or customer problem only when it reaches a certain scale or frequency, software can find errors that happen to even just one customer, such as a fee that’s been miscalculated or a double payment to a credit card. The customer can then be alerted about the mistake and informed that it has already been corrected; this kind of preemptive outreach can dramatically boost customer satisfaction. Banks could also proactively reach out to customers whom predictive modeling indicates are likely to call with questions or issues. For instance, if a bank notices that its older customers have a tendency to call within the first week of opening an account or getting a new credit card, an AI customer service rep could reach out to check in.

Banks have always functioned with an organizational trinity: front offices (branches), middle offices (call centers), and back offices (operations). In the next ten years, this trinity will evolve dramatically. As we’ve already noted, back offices will slim down. Call centers will all but disappear due to AI bots and automation, and branches will be scaled down in number and transformed in function. As more customer transactions move to digital channels, front-line branch employees will operate as skilled personal advisors, helping customers get answers to complex questions that can’t be addressed digitally, giving advice about bank products and features, and generally serving as a one-stop-shop for customers in need across journeys. This is a new paradigm in which customers will receive personalized advice, relying on a simpler organization.

Today’s operations employees are unlikely to recognize their future counterparts. Roles that previously toiled in obscurity and without interaction with customers will now be intensely focused on customer needs, doing critical outreach. They will also have tech, data, and user-experience backgrounds, and will include digital designers, customer service and experience experts, engineers, and data scientists. These highly paid individuals will focus on innovation and on developing technological approaches to improving in customer experience. They will also have deep knowledge of a bank’s systems and possess the empathy and communication skills needed to manage exceptions and offer “white glove” service to customers with complex problems.

To thrive in a world where once-siloed roles like loan closing and fulfillment, compliance, and risk management become an integral part of product development, product management, and customer experience, banks will need to make major organizational changes. They will need to rethink how the people who make the bank run are going to function. This calls for three major efforts:

Develop a plan to migrate to a journey-based organization: Today, functions such as call centers, payments processing, and risk underwriting are organized by product or segment. As banks increasingly focus on personalized interactions, a journey-based operating model will be required. With a journey-based model, banks will ensure operations resources own the customer inquiry or problem until it is solved. A journey-based model will integrate resources with different capabilities and knowledge and will cut across the currently established siloes. To do this, banks will need to re-think how they staff, measure, and track performance, and ultimately deliver to customers.

Design and implement a new talent model: Operations employees in 2030 will need to know how to code, develop products, and understand data, but they will also need the personal warmth and insight to manage exceptions and deal with complex customer problems. To attract this kind of talent, banks will need to expand their geographic footprints and identify talent pools with the required skills and attributes. They will need a new hiring approach to assess and hire talent for operations with different skills from those required today. Finally, banks will need training approaches to develop not only technical skills, but also empathy and the ability to impress customers in every single interaction.

Build a roadmap to accelerate digitization: Banks need to act now to develop an aggressive tactical roadmap that outlines the plan for digitization and automation. Banks that lack a clear long-term automation plan—one that will result in a fully digital operation a decade from now—will struggle to meet customer expectations.

The future will look very different for banks and their customers in 2030. Banks have a unique opportunity to lay the groundwork now to provide personalized, distinctive, and advice-focused value to customers.

Scale advantages are emerging for the largest US banks; their regional peers need to build highly efficient delivery models in order to compete.